Stablecoins for B2B payments in India: hard, but not impossible

Why direct stablecoin settlement runs into a regulatory wall in India and how a hybrid architecture solves it.

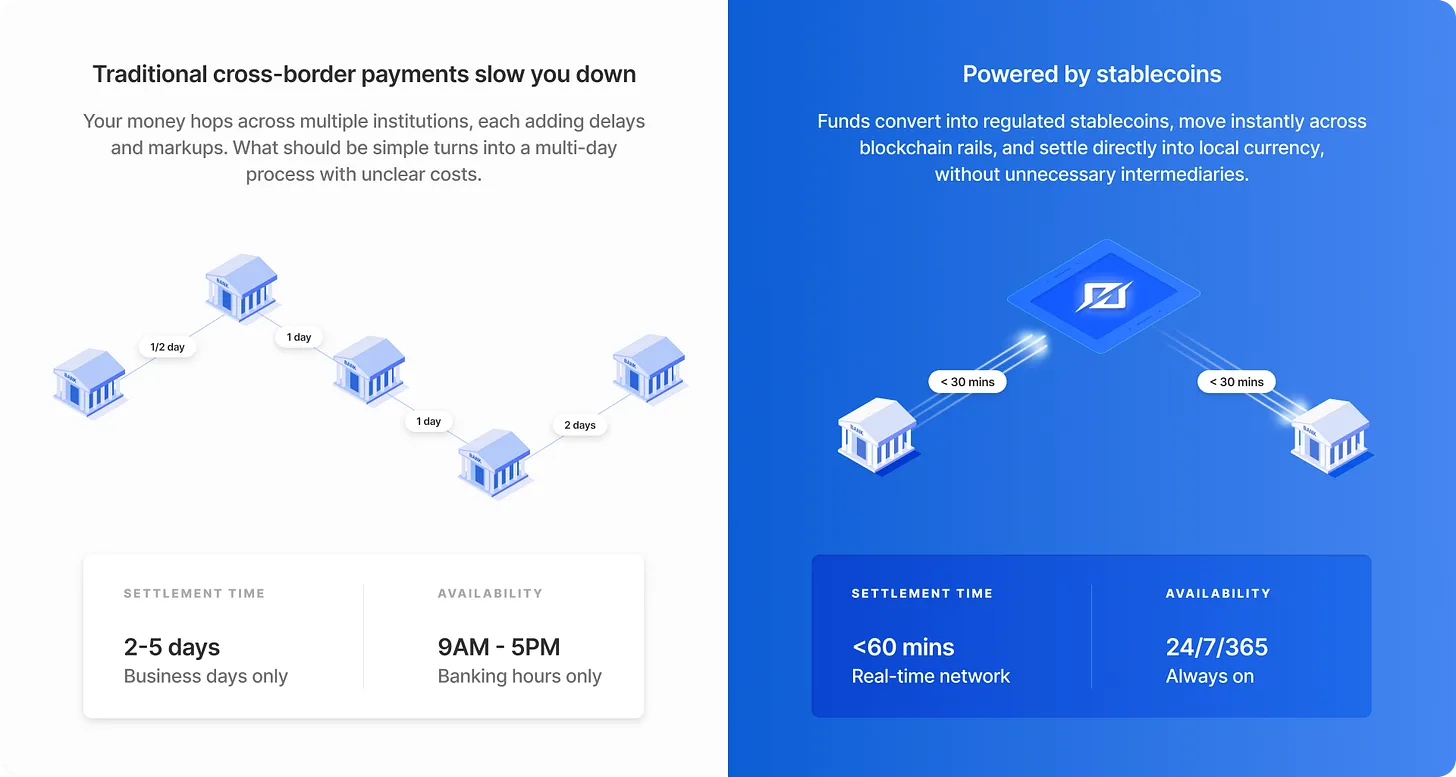

Cross-border B2B payments have been a pain point for Indian businesses for decades.

Traditional banking rails are slow, expensive, and opaque. Stablecoins promise instant settlement, low fees, and 24/7 availability. On paper, the upgrade is obvious.

In practice, direct stablecoin settlement for B2B transactions in India runs headfirst into a fundamental regulatory hurdle.

The answer isn't to abandon stablecoins. It's to understand India's foreign exchange documentation requirements and design payment flows that get the best of both worlds.

Understanding India's foreign exchange documentation

At the centre of this is India's foreign exchange management framework, governed by the Foreign Exchange Management Act (FEMA).

When foreign currency enters India through the banking system, businesses must obtain specific documentation to prove the transaction is legitimate. That documentation is essential for income tax filings, GST input credit claims, export incentive schemes, and regulatory audits.

The two primary documents are the Foreign Inward Remittance Certificate (FIRC) and the Foreign Inward Remittance Advice (FIRA). They serve similar purposes, but they carry very different regulatory weight.

FIRC

An FIRC is issued by Authorized Dealer (AD) banks — institutions like HDFC, ICICI, and SBI that are explicitly licensed by the RBI to deal in foreign exchange. FIRCs are generated when foreign currency is credited into an Indian bank account through traditional channels like SWIFT.

They're typically required for:

Export proceeds (SaaS subscriptions, consulting services, physical goods)

Foreign investment inflows (FDI, convertible notes, equity)

Foreign grants or donations

Any overseas income routed through correspondent banking

What makes a FIRC valuable is the information it contains: proof that the money originated outside India, the exact amount and currency, sender details, and — critically — a purpose code that classifies the transaction under FEMA. That purpose code determines everything from tax treatment to whether the transaction complies with sectoral caps on foreign investment.

FIRA

FIRA emerged as fintechs and payment aggregators began moving cross-border flows outside traditional banking channels. When an Indian SaaS company receives payment through Stripe, or a freelancer gets paid via PayPal, a traditional FIRC often isn't issued — because the money flows through payment intermediaries rather than directly through correspondent banks.

In those cases, a FIRA serves as supporting documentation — essentially an advice note confirming a foreign inward remittance occurred.

The distinction matters

FIRCs carry more regulatory weight because they come from RBI-regulated AD banks. FIRAs, while increasingly accepted, can also be issued by non-banking payment intermediaries, and may face additional scrutiny during tax audits or regulatory reviews.

For high-value B2B transactions, businesses generally prefer FIRCs for the certainty they provide.

The stablecoin dilemma

This is where stablecoins hit a wall in the Indian B2B context.

When USDC or USDT arrives in India via blockchain rails, it needs to be converted into rupees before it can be transferred to the beneficiary's bank account. The regulatory classification of that conversion is the problem.

Technically, converting USDC or USDT into INR is a domestic transaction — a cryptocurrency sale happening within India's borders. From the regulator's perspective, it doesn't qualify as a foreign inward remittance because no foreign currency has entered the Indian banking system through recognized channels.

So no FIRC or FIRA is generated.

For the receiving business, this creates an impossible situation. They have rupees in their account, but no documentation proving those rupees originated from a foreign source. Which means:

No GST input credits on export services

No demonstration of compliance with export obligations

No clean paperwork for income tax filings

A straightforward B2B payment turns into a compliance nightmare.

And this isn't hypothetical. Indian tax authorities and GST departments actively verify FIRCs during audits. Export-oriented businesses rely on these certificates to claim duty drawbacks and other incentives. Without proper documentation, even legitimate foreign earnings can get questioned — leading to disputes, penalties, and frozen incentives.

A hybrid architecture that works

The fix isn't to abandon stablecoins. It's to use them as a settlement layer while keeping compliant documentation at the last mile.

The architecture is straightforward.

Take a US-based merchant (Merchant A) paying an Indian supplier (Merchant B) for services rendered.

The traditional model: Merchant A initiates a SWIFT transfer. It settles in 2–3 business days, incurs 2–6% in fees between forex conversion and intermediary charges, and gives almost no visibility into where the payment is in the pipeline.

The stablecoin-hybrid model: Merchant A sends USDC or USDT to us. We operate both blockchain infrastructure and an Authorized Dealer bank account in India.

Here's how it flows:

We fund a nostro account with an equal amount of USD.

The moment we confirm the stablecoin transaction has been initiated on-chain (not necessarily fully settled), we trigger an INR transfer from a vostro account at our AD bank to Merchant B's Indian bank account.

Merchant B receives rupees from a regulated bank with a proper FIRC documenting the foreign origin of funds — sender details, amount in original currency and INR, correct purpose code, all of it.

That satisfies every regulatory requirement for tax compliance, GST claims, and FEMA documentation.

Meanwhile, we manage the blockchain settlement risk and currency liquidity on our side. We maintain enough INR reserves to front payments while stablecoin settlements complete, and we handle the conversion through compliant channels.

Stablecoins give us fast, low-cost international settlement between the US merchant and us. The traditional banking system handles the last mile into India, with full documentation.

The value proposition

This model delivers improvements on three fronts:

Fully compliant. The Indian merchant receives funds through a regulated AD bank and gets legitimate FIRCs that will hold up to any audit.

Faster settlement. Compresses from 2–3 business days to same-day — sometimes hours. Better cash flow, better working capital management.

Lower cost. The expensive SWIFT leg gets replaced by efficient stablecoin transfers. At scale, we can offer more competitive rates by managing currency liquidity centrally.

Maybe the most important part: this model abstracts the complexity away. Merchants don't need to understand blockchain, manage crypto wallets, or navigate the regulatory ambiguity around digital assets. They interact with familiar banking interfaces and receive standard documentation. Stablecoins work invisibly in the background, making the system faster and cheaper.

The bigger takeaway

Stablecoins won't replace traditional payment rails in India entirely — the regulatory framework doesn't allow for it yet.

But they can power a new layer of financial infrastructure that combines the speed of blockchain settlement with the compliance and documentation of regulated banking. As this model matures, it could reshape how businesses think about cross-border payments.

Not as a choice between compliance and innovation — but as a chance to have both.