Understanding stablecoin premiums in India

If you've been exploring stablecoins for cross-border payments in India, you've probably heard whispers about "premiums." Here's what they actually are, why they matter, and why you shouldn't build your revenue model on them.

Some folks treat premiums like discovering buried treasure. Others have built entire business plans — complete with detailed spreadsheets — around them. (We've seen the decks.)

Here's the thing: premiums are a useful way to explore the stablecoin space, but they're not something to anchor a business on.

What are premiums?

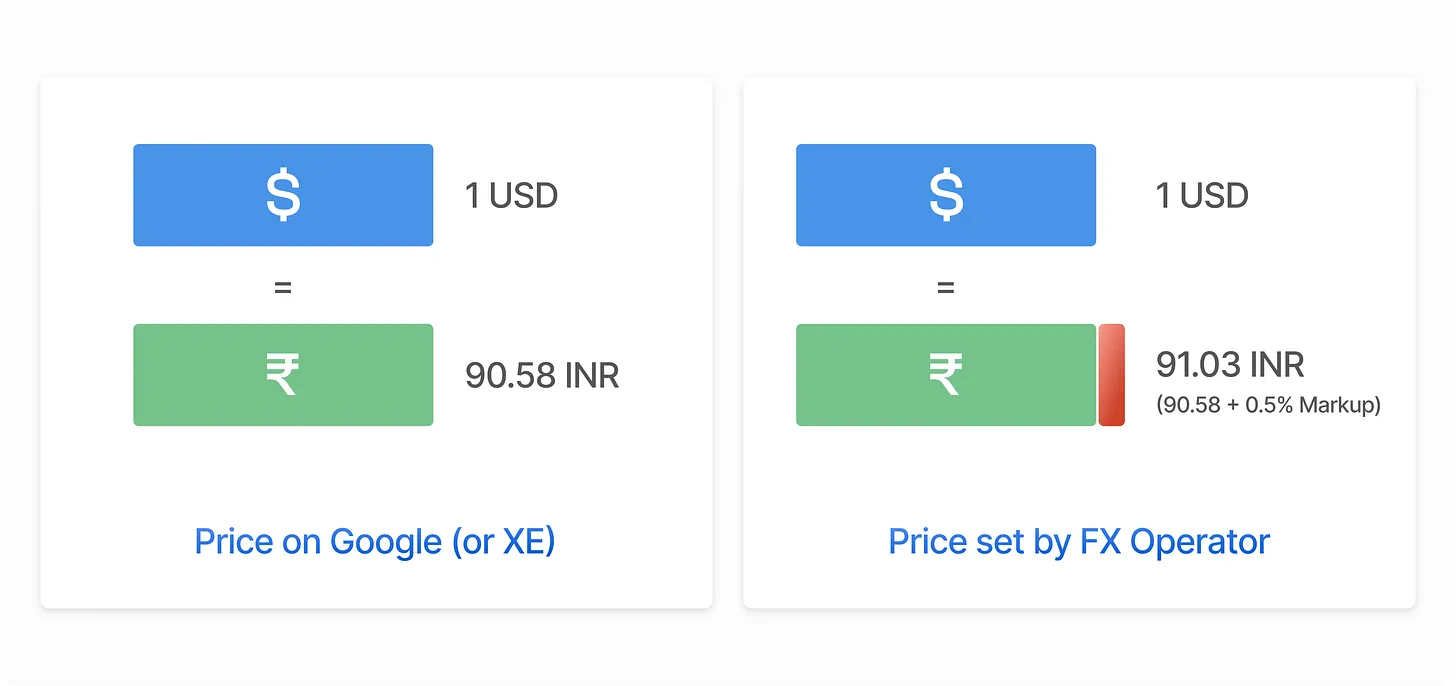

Put simply, a premium is the markup you pay above the "official" exchange rate when you actually convert currency — whether through a bank, a money changer, or a stablecoin.

Why does this exist?

In countries with relatively less valued currencies, it typically costs more to buy a global standard currency like the US dollar.

For example: if 1 USD costs ₹90.58 on Google or XE, an FX operator might charge ₹91.03 to sell you 1 USD — a 0.5% markup over the reference rate. That difference is their margin.

The same logic applies to USD-backed stablecoins. They offer something valuable in constrained environments: easy access to dollar exposure.

When getting USD through traditional banking involves regulatory hoops, multi-day approvals, or capital control limits, people will pay a little extra for the stablecoin version.

It's just supply and demand doing its thing.

The premium rollercoaster in India

If you've been tracking Indian stablecoin premiums over the last few years, you've probably noticed they're about as predictable as Bangalore weather.

Back in 2023, premiums of 4% weren't uncommon. India had tighter capital controls, fewer regulated on-ramps, and stablecoins represented a genuinely scarce form of dollar access.

Fast forward to 2026, and the story has changed dramatically. As registered exchanges entered the market, market makers improved liquidity, and large remittance flows added consistent supply, premiums compressed hard. We've even seen periods where they flipped negative.

Today, under compliant conditions, the realistic premium in India hovers around 1–1.5% on good days, and 0.4–0.8% on the rest. Sometimes it spikes over weekends or banking holidays when local rails slow down. Sometimes it disappears entirely.

The only constant is change.

Yes, premiums will stick around but not how you think

Premiums won't disappear completely, and that's actually normal.

Traditional FX businesses and money transfer operators have been making money on spreads for decades. The bid-ask spread is how markets work — even in the most liquid currency pairs, there's always some difference between buying and selling prices.

The same applies to stablecoins. As the Indian market matures, you'll see persistent but smaller spreads — think 0.5–1% in normal conditions, not the 3–4% wild-west days.

That's how healthy markets compensate liquidity providers and operators for their service. The real question isn't whether premiums will exist. It's whether you're building your business model on realistic expectations, or chasing under-the-counter premiums.

When premiums are too good to be true

Now for the uncomfortable part.

If someone is promising you sustained 3–4% premiums in India right now, you should be asking hard questions. Starting with: where is this liquidity coming from?

The reality is that those fat premiums often come from somewhere sketchy. Some OTC desks and stablecoin payment providers source their liquidity from channels that most legitimate operators would never touch — the kind of flows that look great on a pricing sheet but leave a paper trail you don't want attached to your business.

Why do they offer better rates? Because they're taking risks you probably don't want any part of.

Using this kind of liquidity might feel like a great deal today, but it can come back to haunt you months later:

User account freezes

Banking partner liens

Regulatory notices

Reputational damage that's impossible to undo

No fintech operator can afford license suspension or regulatory scrutiny for marginal upside on a single transaction. The upside doesn't justify the downside.

And in India's increasingly regulated fintech environment, cutting corners on compliance is a losing bet — with regulators, with banking partners, and with users.

Build on solid ground

Bottom line for fintech operators: premiums are great for kickstarting a cross-border business using stablecoins. They can provide a nice margin during early corridor development. They make the unit economics look really attractive in that first investor deck.

But — and this is a big but — your unit economics can't be built solely on premiums. They're too volatile, too dependent on market conditions, and very likely to compress as the market matures.

Instead, think of premiums as a market signal:

When they're high, it tells you there's an access problem worth solving.

When they compress, it tells you the market is getting more efficient.

Both are useful information. Neither is a sustainable moat.

Build your business on operational efficiency, regulatory compliance, superior UX, and network effects. Let premiums be the cherry on top — not the cake.

How Saber approaches this

At Saber (part of Mudrex), we've made a deliberate choice: we only work with verified OTC desks and exchanges that are FIU (Financial Intelligence Unit) compliant to buy and sell stablecoins.

Is it slower sometimes? Yes.

Do we occasionally miss out on slightly better rates? Maybe.

But do our partners sleep well at night knowing their liquidity sources are clean and their users' accounts won't get frozen six months later? Absolutely.

In a market that's still finding its regulatory footing, compliance is what actually matters.