Asia's (strong) case for stablecoins

In our last post, we introduced Saber. This one's about why we chose Asia and why, if you run a fintech that moves money from the world into this region, you should care.

Asia is the region where cross-border payments are most broken, and most ready to be fixed.

Ironically, domestic payments here are already world-class.

The complexity of sending funds to Asia

Asia's cross-border payment landscape is a maze of currencies, regulators, and disconnected systems. For millions of migrants from India, Indonesia, the Philippines, and beyond, sending money home is still slow and expensive. And the startups serving them are stuck solving the same plumbing problems, over and over.

The scale of the flow is staggering:

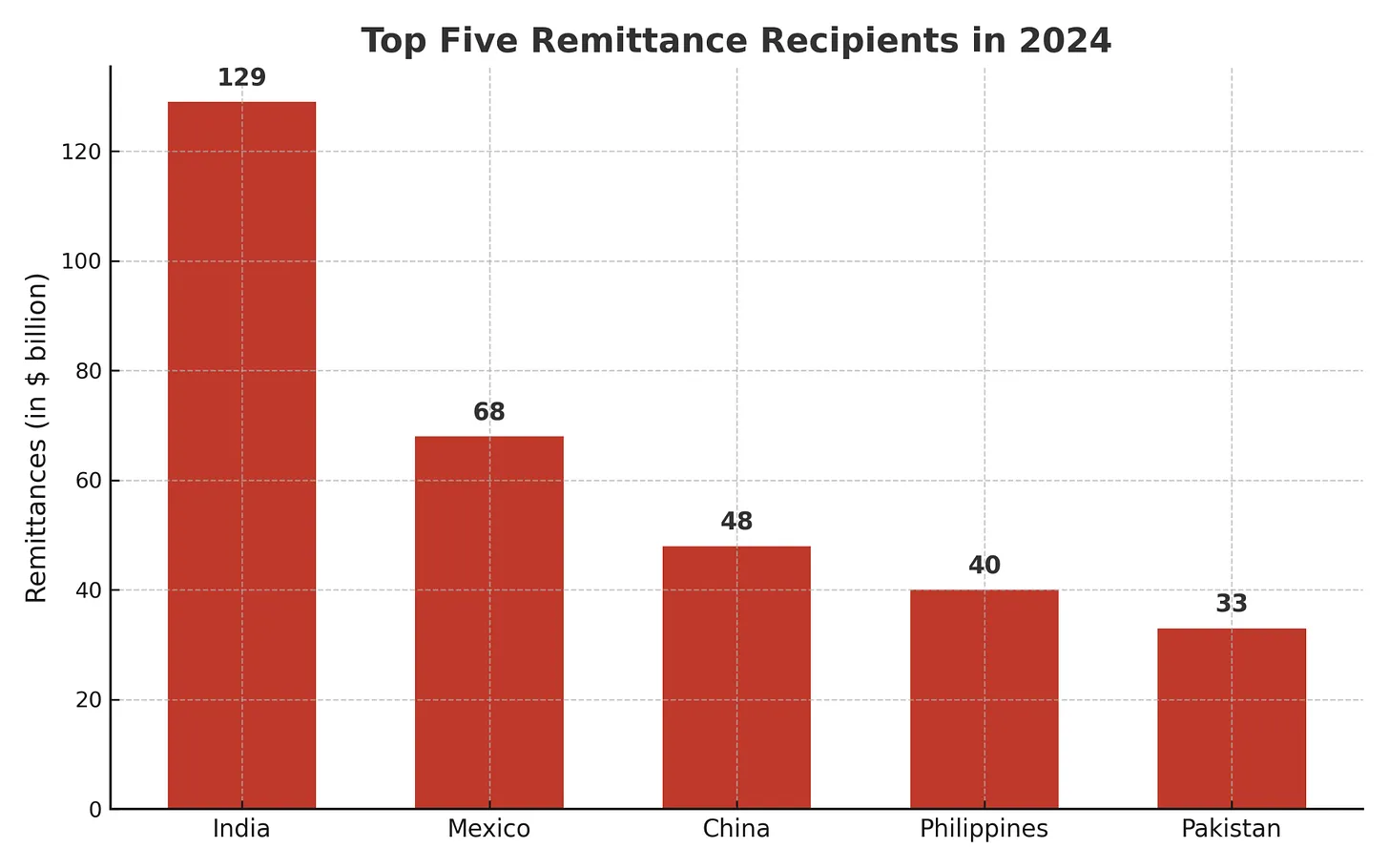

India received $129 billion in remittances in 2024 — the highest in the world.

The Philippines pulled in $40 billion.

Indonesia received $14 billion.

Four of the top five remittance recipients globally are Asian countries.

In smaller economies like Nepal, these flows can make up close to 20% of GDP. They sustain families and prop up national balance sheets.

And yet the cost of getting money here is steep.

Sending a small amount like $200 to a low- or middle-income country costs around 6% in fees. Some corridors push closer to 10%, especially from Western markets. On top of that, transfers can take days to clear, thanks to the SWIFT network and its stack of correspondent banks.

That friction pushes a huge chunk of volume into informal channels — hawala networks, cash couriers. The IMF estimates up to half of global remittance flows go unrecorded.

The system is overdue for a rewrite.

A fragmented landscape

Unlike Europe's SEPA, Asia has no unified payments framework. Every corridor has its own compliance rules, capital controls, and FX hurdles.

India's cautious stance on crypto sits alongside the Philippines' openness to fintech innovation. Singapore, Japan, and Hong Kong are actively regulating private stablecoins. China and India are pushing their own CBDCs. The result is a regulatory patchwork that makes scaling cross-border products genuinely hard.

Here's the irony: domestic payments in Asia are some of the best in the world. India's UPI, Singapore's PayNow, QR-based wallets across Southeast Asia, all fast, ubiquitous, nearly free.

They just stop at national borders.

A Thai tourist still can't easily pay an Indonesian merchant using their local wallet. Initiatives like Project Nexus aim to connect instant payment systems across the region, but full implementation is still years away.

Until then, Asia's cross-border transfers remain slow, opaque, and expensive.

This is a gap fintechs can actually fix today.

Why stablecoins?

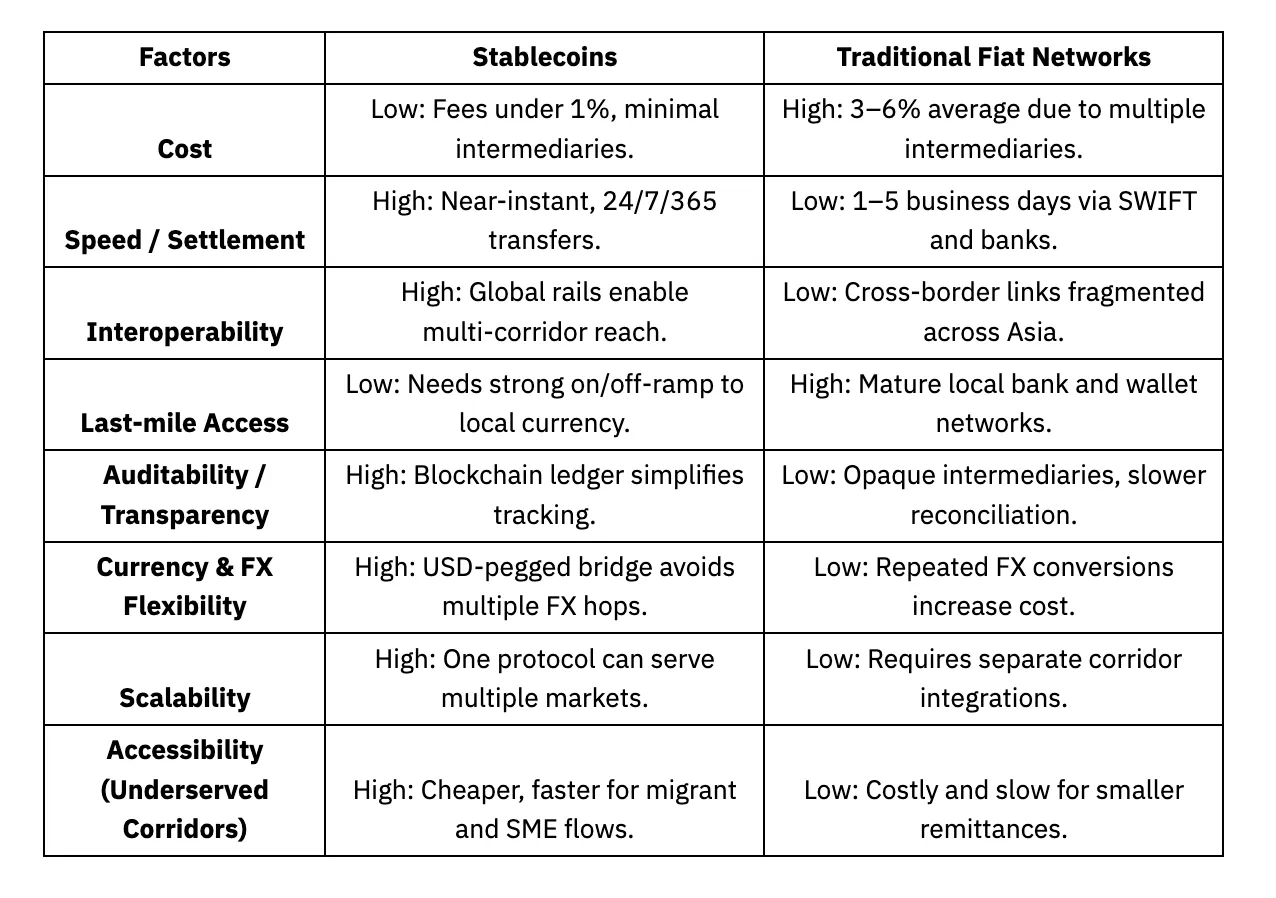

Stablecoins — digital currencies pegged 1:1 to fiat like the USD — are the most obvious path to this fix.

A digital dollar moves instantly, 24/7, across borders, for negligible cost. An Indonesian worker in California can send $100 in USDC to her family in Jakarta, who receive it in seconds and cash it out in rupiah. No SWIFT. No correspondent bank chain.

Stablecoins already power trillions in global payments, increasingly well beyond crypto trading.

But the catch is the last mile — the on- and off-ramps between stablecoins and local fiat.

On-ramp: local currency → stablecoin.

Off-ramp: stablecoin → local currency.

Without reliable bridges on both ends, recipients still can't access or spend their money.

The technology works. The infrastructure around it often doesn't.

That's the gap.

The Saber approach

This is where Saber comes in.

We're building a payment network that combines the speed of stablecoins with the reliability of fiat. Our platform lets companies on-ramp local currency into a stablecoin, move funds globally, and off-ramp back into local currency — all on a single rail.

We've tackled the hard parts first:

Regulatory registrations across 10+ markets — India (FIU), UK (e-money license), Canada (MSB), Australia (AUSTRAC), Dubai (VARA), Indonesia (OJK), Philippines (VASP), and more.

Rails covering 40+ countries and 10+ currencies.

Local payment integrations — India's IMPS, Indonesia's clearing networks, and equivalents across the region — connected to global stablecoin liquidity.

For the companies building on top of us, all of that complexity is invisible. Transfers settle in seconds. Fees drop dramatically. Payouts land through familiar channels — bank deposits, e-wallets, and more.

We've already processed over $1.5 billion in annualized volume working with some of the largest remittance companies and fintechs in the region.

One thing we've learned the hard way: in Asia, compliance isn't optional. It's the foundation everything else sits on. Our rails are compliance-first by design, with KYC and AML controls wired into every market we operate in.

What you can build on Saber

Remittances — Faster, cheaper cross-border transfers.

Global payroll — Instant payroll and vendor payouts, anywhere.

Wallet & exchange integrations — Seamless fiat–crypto conversions.

Emerging verticals — Gaming, digital commerce, and cross-border creator payouts.

The bottom line

Stablecoin speed. Fiat accessibility. Regulatory rigor. Saber is stitching these together into the connective tissue for Asia's next-generation payment infrastructure.

The long-term vision is simple: make geography irrelevant for money movement. Whether you're paying a supplier in Vietnam or sending money home to India, transfers should be instant, affordable, and transparent.

The pipes are being laid. The rails are live. The future of Asian cross-border payments is already being rewritten.

That's why we do what we do.